Guides

CAISO Storage Operations: The Complexity of Doing it Well

Guides

Everything you need to know about CAISO’s EDAM and DAME, and its implications for energy storage operators.

The Extended Day-Ahead Market (EDAM) and Day-Ahead Market Enhancements (DAME) are scheduled to go live in CAISO on May 1, 2026.

For years, the Western Energy Imbalance Market (WEIM) has enabled real-time trading across balancing authorities (BAs). EDAM takes that coordination one step further — extending participation into CAISO’s Day-Ahead Market (DAM) and introducing new products designed to manage uncertainty and reliability at a regional scale.

For battery operators in CAISO — and for utilities and asset owners across the Western Interconnection — this marks a structural shift in how value is created and captured in day-ahead markets.

Today, WEIM allows BAs to trade real-time energy across borders. Since its inception, WEIM has grown from two to 23 participants, covering roughly 80% of the West’s load and generated an estimated $6.25 billion in gross benefits.

EDAM extends this model into the DAM.

Instead of planning generation and load largely within individual balancing authorities, EDAM will enable a coordinated DAM across participating BAs. The goals of this initiative are threefold:

In parallel, CAISO is introducing Day-Ahead Market Enhancements (DAME), which introduces two new DAM products designed to address supply uncertainty and reliability needs across the expanded regional footprint.

Designed to proactively manage uncertainty between the Day-Ahead and Real-Time markets by incorporating expected net load variability directly into the DAM.

As solar and wind penetration increases, differences between DA schedules and RT conditions have grown. Historically, these imbalances were addressed primarily through the RUC process and out-of-market actions. IR brings that uncertainty into the DAM and co-optimizes it alongside energy and ancillary services.

Importantly, if a resource is economic for energy but held back to provide IR instead, DAM pricing is designed to compensate it for the opportunity cost — making the resource economically indifferent between providing energy and IR.

Designed to address differences between cleared physical supply in the DAM and updated load forecasts – and enhance the RUC process by ensuring sufficient incremental and decremental capacity is available to meet differences between cleared physical supply and updated load forecasts.

These products are intended to manage uncertainty more explicitly in the day-ahead — where CAISO strives to procure all needed capacity, and reduce the need for last minute, out-of-market actions.

For batteries already operating in CAISO, EDAM changes the competitive landscape in a few ways:

More participants in the Day-Ahead Market means more supply. Conceptually, it makes sense that increased supply (and supply diversity) would push prices lower – and that is what happened with the introduction of the Western Energy Imbalance Market (WEIM). The greater region coordination increased efficiency and lowered price spreads.

However, the effect will vary across products and hours. There will still be an optimal product and widest spread to be captured. Operators looking to maximize revenue and grid impact will be challenged to forecast and capture these opportunities.

At Tyba, we leverage Dynamic Price-Quantity (PQ) Bidding to help ensure we clear the most capacity into the highest priced products in their highest priced intervals. The model places tiered bids, where we offer a specific number of megawatts if prices clear in a specific price range, to ensure our awards align with actual prices.

The introduction of Imbalance Reserves (IR) and Reliability Capacity (RC) need to be accounted for pre-DAM bid submission calculations. From what we have seen in other ISOs when new AS products are introduced – for example, ECRS in ERCOT – we can hypothesize that most volatility will happen in the weeks after implementation, but will reach equilibrium in the long run.

A dynamic bidding strategy is also imperative here – so you can take advantage of early volatility and clear into high priced moments without tying up the asset more than is beneficial.

Today, CAISO’s resource mix is increasingly dominated by renewables – with solar making up the largest portion of that at more than 17 GW on the grid. This leads to specific pricing trends, and specifically opportunities for storage to jump into action during the morning and evening hours when the sun is just coming up / going down and production is fluctuating. It also drives low or even negative midday prices that can be great opportunities to recharge.

The other BAs participating in EDAM, though, will shift this mix, bringing much more natural gas and coal. Since these types of plants are only restricted by startup and operating costs, not nature, it is likely they will further heighten DAM competition. In the same way we saw thermal generators take advantage of the high Non-Spin prices when ERCOT introduced a longer associated duration requirement with the launch of RTC+B, we will likely see these resources more able to be long DA since they don’t have to worry about generation risk.

Guides

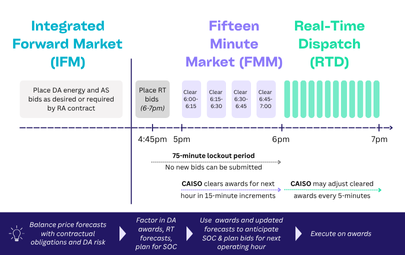

Demystifying CAISO’s bidding timelines

10/21/25

Guides

A Trader’s Guide to Controlling Storage Optimization Strategy

09/03/25

Guides

Operating Storage in ERCOT vs. CAISO

10/08/25

Guides

Path to Go-Live: Key Steps for Storage Assets in CAISO

09/23/25

Guides

08/09/23

Case Studies

[Case study] Grid-Enhancing Optimization with White Pine Renewables & PG&E

11/18/25

Guides

CAISO Storage Operations: The Complexity of Doing it Well

Guides

Demystifying CAISO’s bidding timelines

10/21/25

Guides

A Trader’s Guide to Controlling Storage Optimization Strategy

09/03/25

Guides

Operating Storage in ERCOT vs. CAISO

10/08/25

Guides

Path to Go-Live: Key Steps for Storage Assets in CAISO

09/23/25

Guides

08/09/23

Case Studies

[Case study] Grid-Enhancing Optimization with White Pine Renewables & PG&E

11/18/25